Top 5 Themes Keeping Us Awake in 2022!

By Carl Paraskevas - Chief Economist

COVID MATTERS LESS NOW

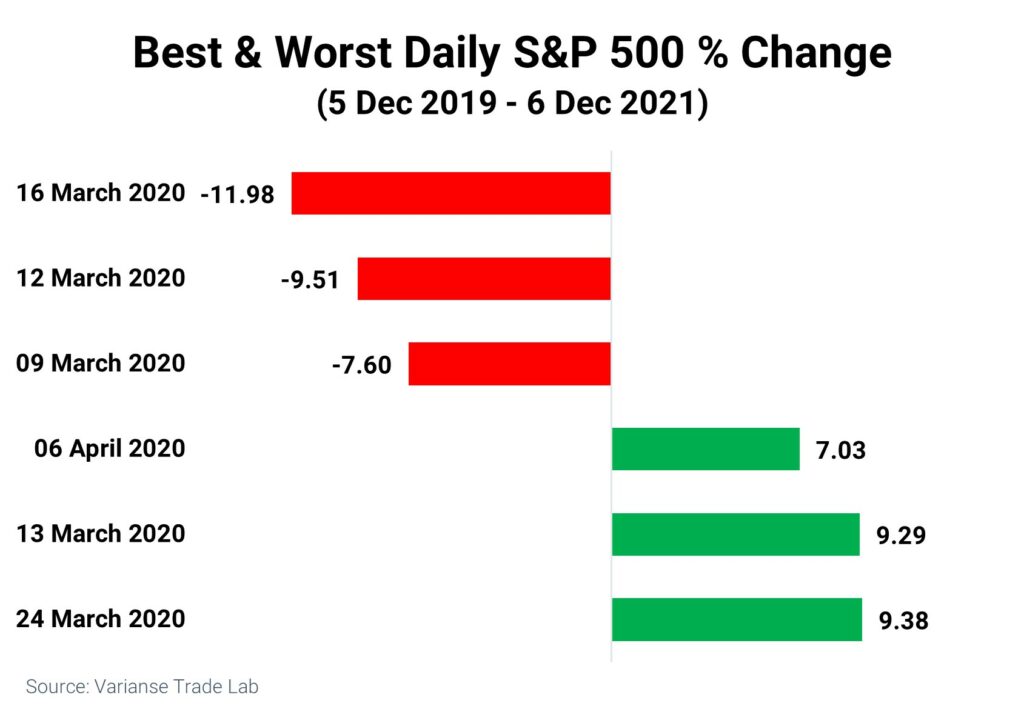

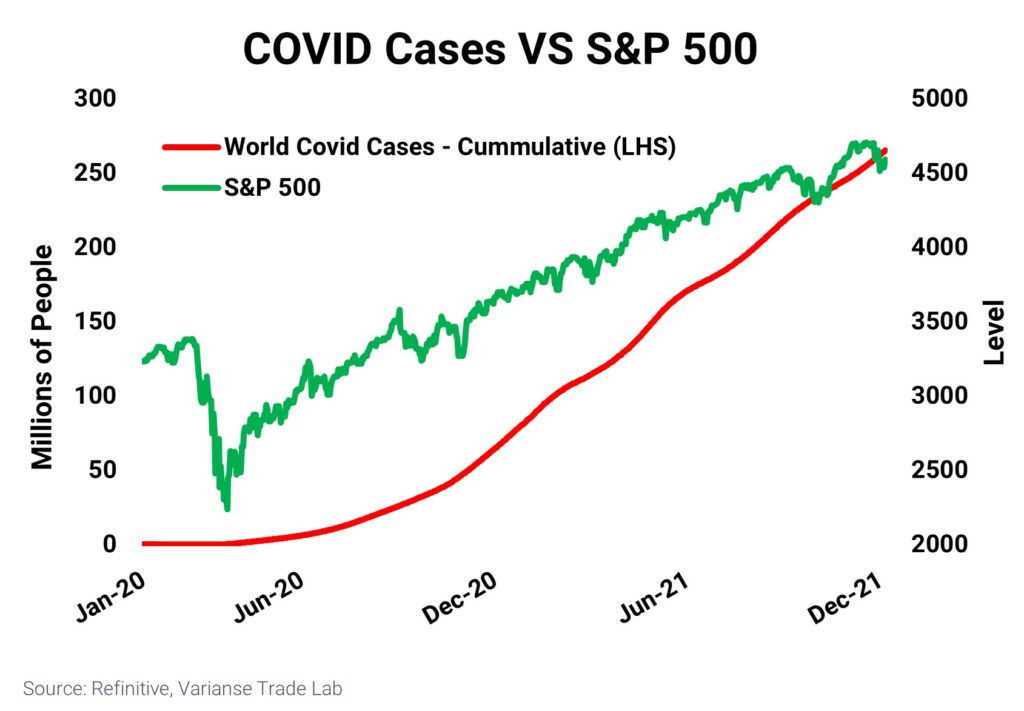

If we’ve learnt anything from the new Omicron variant, it’s that COVID in one form or another will be here to stay. Nature guarantees future mutations of the virus but leaves their timing and lethality to chance. Such uncertainty can be nerve wrecking for those trading financial markets. News of Omicron, for example, wreaked havoc across various markets on the 26 November of this year with the S&P 500 closing c. 2.3% lower on the day.

Yet we’ve seen bigger negative reactions earlier in the pandemic. For example, during March of 2020, when the US and UK first started to introduce travel bans and lockdown restrictions, the S&P 500 recorded two daily drops in excess of 10%. Likewise, we’ve witnessed the S&P 500’s meteoric rise from a low of 2,919 in March 2020 to November’s record high of 4,743 even as cumulative cases of COVID-19 rose in the background.

THINGS LOOK BRIGHTER

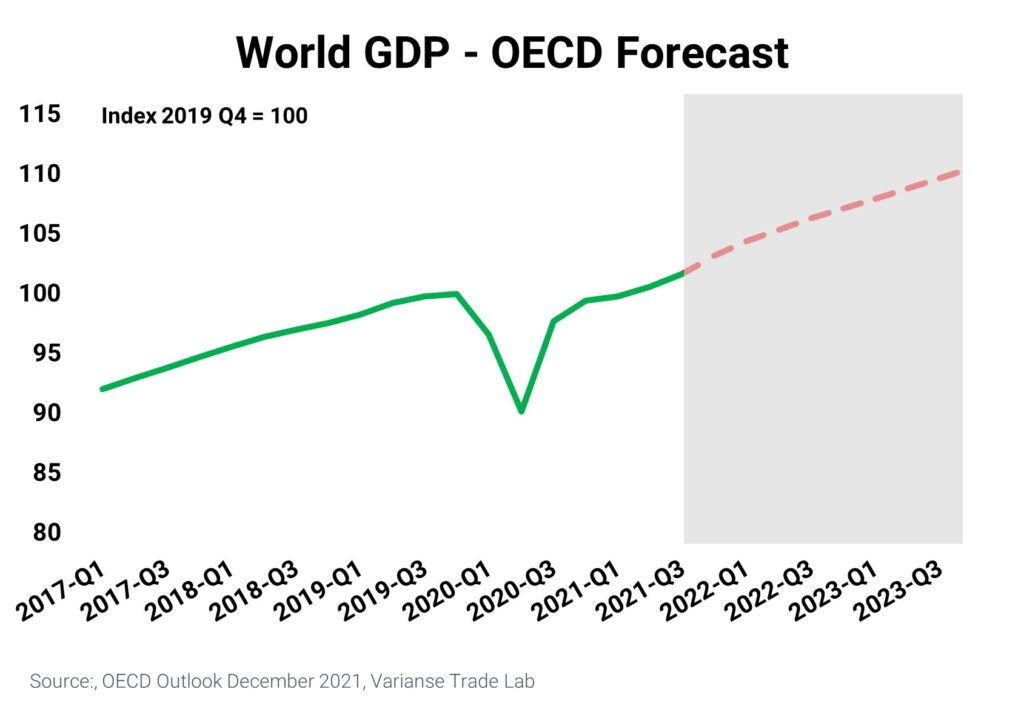

Suffice to say, markets have moved on since the early days of the pandemic. Vaccines, new treatments, unprecedented monetary loosening from the world’s central banks and major fiscal support from developed governments have all led to a sharp recovery in economic activity. According to the latest figures from the OECD, the world’s GDP has now officially surpassed its pre-pandemic levels.

That’s certainly good news for the world, but it does not necessarily make life easier for traders. In many respects, the first two years of COVID brought with it predictable risk-on and risk-off opportunities, whereas 2022 may prove nowhere near as black and white.

Still, one thing is for certain, just as the reaction to the global financial crisis defined the market landscape for much of the last decade, the reaction to COVID-19 will define the market for the years to come.

Equally, it is important that we don’t lose sight of some of the other structural changes happening in the world play out; the impact of climate change policy, the role of crypto currencies, and the challenge posed to the US by China’s rise are the first that come to mind.

So, if it is not COVID that is keeping us awake at night, then what is?

#1 - THE US DOLLAR

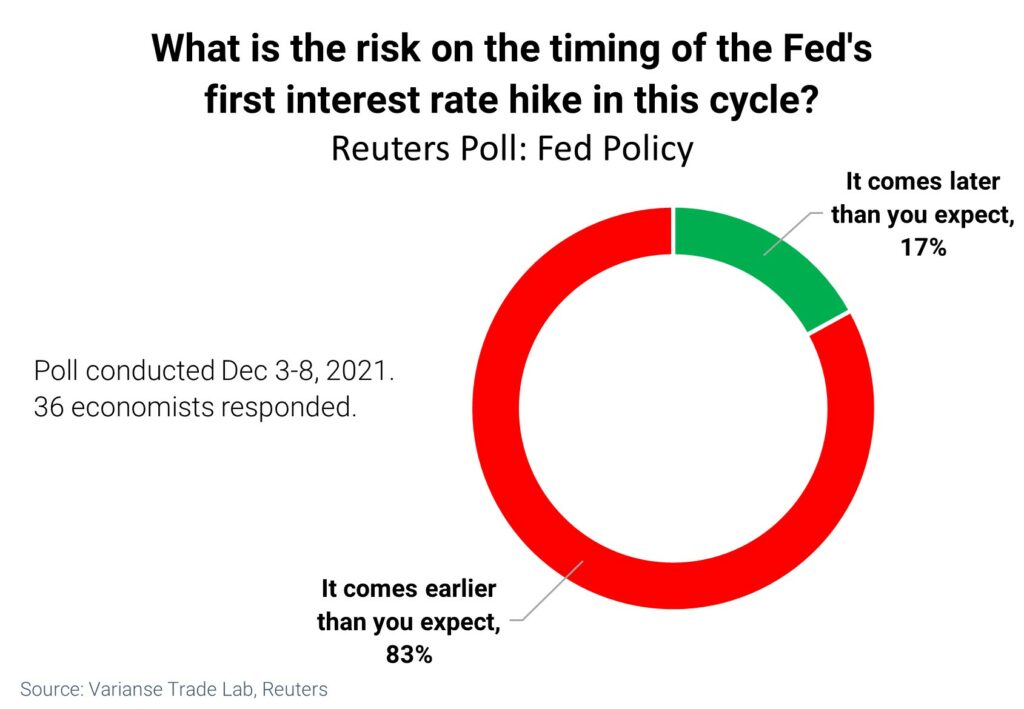

The US dollar was the big winner against most of the major currencies in 2021. Markets were quick to price in the tapering of asset purchase and tighter monetary policy in 2022, lending broad support to the world's reserve currency. At the time of writing, the bond market was pricing in two full 25 bps interest rate hikes from the Fed in 2022, with the first to come in June 2022. Our concern is that both markets and economists have a historic tendency to overestimate both the level and timing of future Fed hikes.

In addition, there are other macro factors at play, which add to US dollar uncertainty, like the widening of the US current account as a percentage of GDP.

#2 - INFLATION

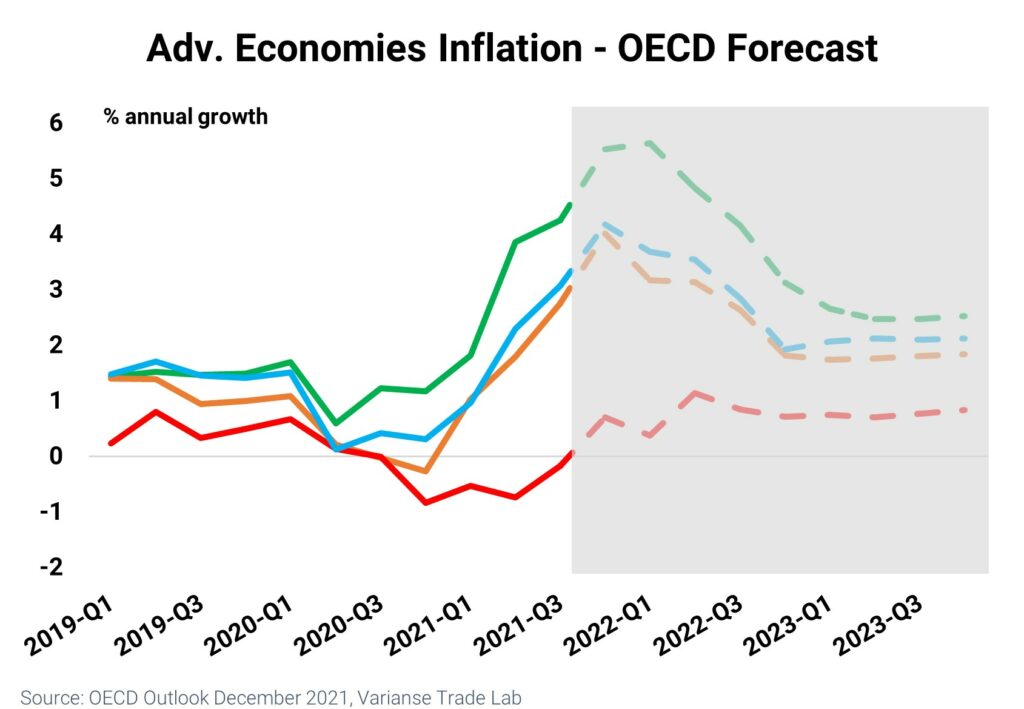

The quick reboot of the global economy came at a cost of higher inflation. Headline US CPI reached 6.2% y/y in October – its highest level since December 1990. Inflation rates in other major economies have also soared. But the world’s major central banks have been going back and forth on whether it is transitory or not.

The economic consensus is that global inflation will peak sometime in Q1-2022, but some of the supply chain issues and commodity prices effects that have lifted inflation rates could persist for much longer. Others point to concerns that today's elevated inflation have shifted upward inflation expectations and seeped into the service sector.

Whatever the situation, elevated inflation is putting pressure on major central banks to tighten policy, and opens up the risk of policy errors. Higher interest rates, accompanied by decent economic growth and tame inflation are good for currencies, but higher rates accompanied by low growth and persistent inflation could prove very negative.

#3 - EMERGING MARKETS

Vaccine inequality has contributed to unbalanced economic recovery favouring rich nations. Without vaccines, emerging markets look vulnerable to more draconian lockdown measures and new COVID variants. Equally, they are at risk to capital flight if developed nations do indeed raise interest rates, albeit less so than in the past.

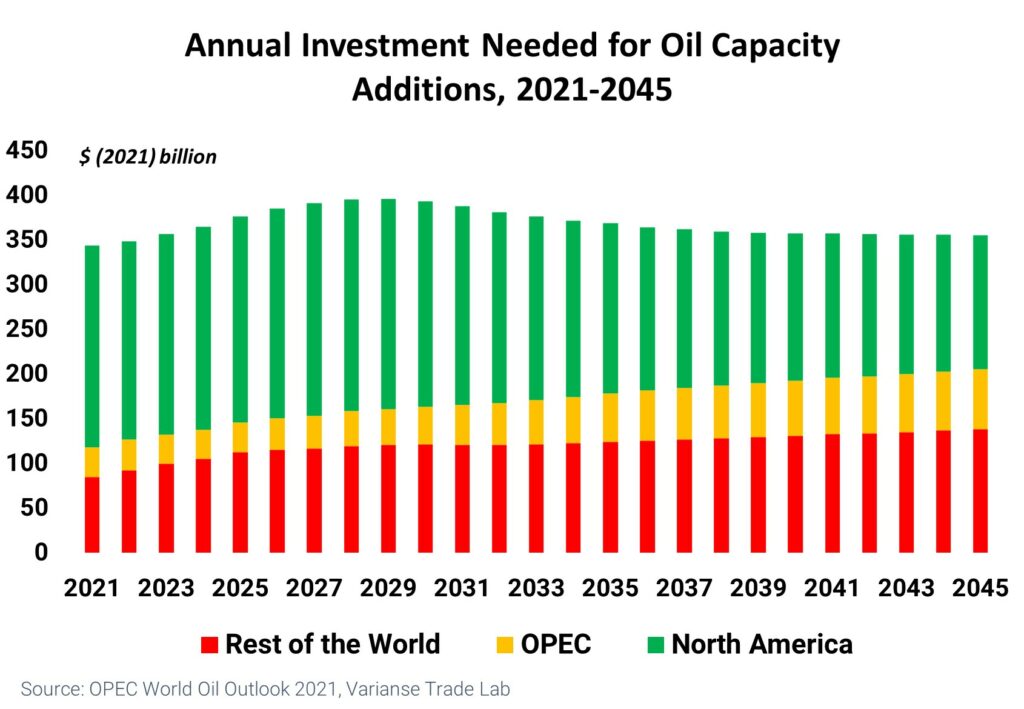

#4 - OIL PRICES

Measures to flight climate change will have an impact on long-term oil demand, but if supply fails to keep pace with existing demand, prices can still rise even as demand peaks and falls. Volatility in oil, but also natural gas has the propensity to stay elevated.

In order to maintain the balance between oil demand and supply, substantial investment will be required to ensure sufficient capacity. Such investment may be less than forthcoming given the recent focus on deterring investment in fossil fuels.

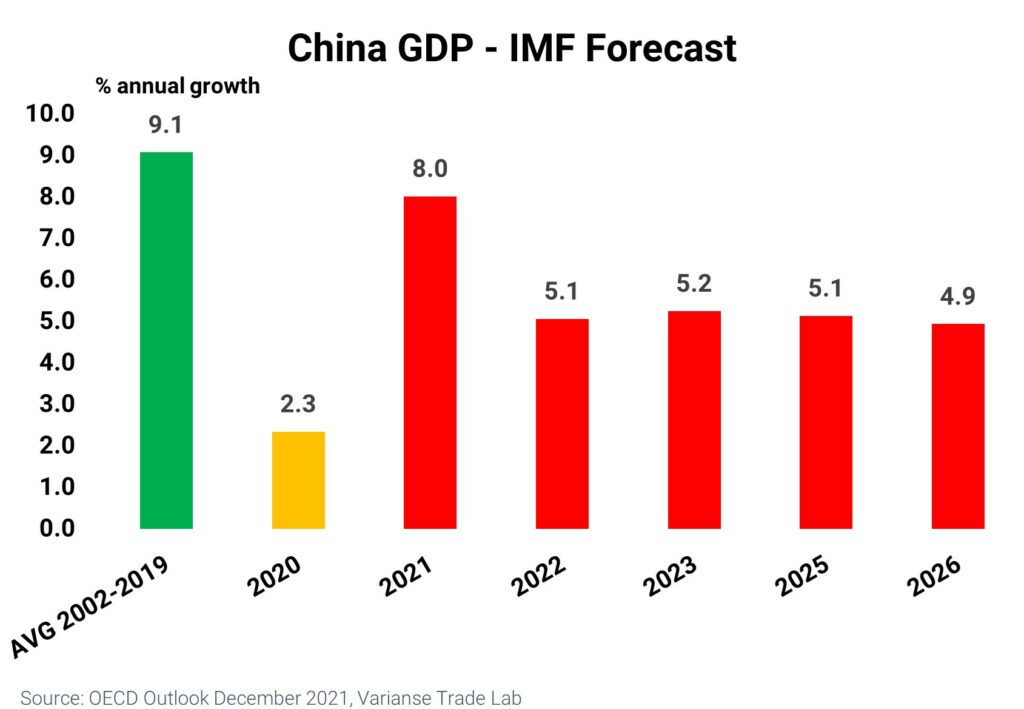

#5 - CHINA

As expected, the long-term pace of economic growth in China is slowing. But economic prosperity has viewed as being one of the areas maintaining social stability. Add in already high levels of total debt to GDP, the crisis in the property development sector, and there are reasons to be cautious. Moreover, it could have unintended geopolitical consequences as tensions between the US and China remain frothy.

Latest News

-

VARIANSE Launches Crypto CFDs

Jan 13, 2023, 3:30 PM

-

An Automated Trading Partnership: ClickAlgo and VARIANSE

Nov 16, 2022, 10:53 AM

-

VARIANSE Is Best Broker for Online Trading UK

Sep 15, 2022, 4:18 PM

-

ECB leaves EUR/USD traders disappointed

Jun 9, 2022, 4:26 PM

-

AUD/USD: keep your eyes peeled on 0.72664

Jun 1, 2022, 11:40 AM

Categories

Your global trading connection

Multi-Award Winning

VARIANSE has achieved consistent recognition from independent organisations and the financial community.

Premium Customer Support

Take comfort in an experienced team committed to providing you with rapid, efficient, and friendly support.

Regulated Globally

VARIANSE is authorised and trusted internationally. We have entities regulated by the FCA, FSC and in SVG.

Tier-1 Banking Relationships

We safeguard your funds safely and securely in segregated ring-fenced client money custodian bank accounts with Barclays Bank.

Join Us and See WhyElite Traders Choose VARIANSE