The CFD vs Spread Betting Journey

CFD vs spread betting - what’s the difference? Back when I was first considering trading, I asked myself that very same question. A lot of my friends, most of them bankers based out of London just like me, were either doing one or the other. Many of them, including myself still do. Yet to this day, when I ask them about the difference, they don't have a coherent answer. Most mumble something about tax differences. When I've probed them a bit more on the subject, it's clear everyone is really clueless. That’s pretty scary stuff when you consider some of them, including myself, trade pretty large position sizes. Lack of a coherent answers around CFDs vs Spread Betting pushed me to try and discover the answers myself. Below I lay bare what I learned along my journey.

Sports Spread Betting

In terms of the history of CFD vs Spread Betting, spread betting is far older, but also a lot seedier concept. The history of spread betting goes back to the first half of the 20th century. Invented by Charles K. McNeil, a US mathematics teacher, who later became a bookmaker in Chicago in the 1940s. McNeil invented a system where gamblers could bet on whether the score of both sides of a sporting event would be more or less than the expected outcome of the bookmaker. Gamblers benefited from a new way to gamble and bookmakers gained new opportunities to make money.

Gradually spread betting would make its way across the Atlantic to the UK. Its popularity would eventually explode in the 1980’s as an alternative to fixed odds betting. Like many transatlantic exchanges, however, UK spread betting took on a much different form than its US cousin. The American version remained very much a fixed stake business, where the payout for spread betters would also be fixed. For example, in the case of an American Football team, where the Jets beat the Jaguars by 5 points more than expected by the bookmaker, then those on the correct side of the spread bet would be paid out the fixed payout and the losers just lose the amount they stake.

Point Based Staking is Born

The UK version, however, morphed into staking based on individual points. Suppose that British football team Tottenham beat Manchester United 4 goals to 2 versus the bookmaker markets expectation of 2 to 1. Someone who placed a £1 stake would have won £1 for the one point difference above the expected spread plus their original stake back. Were Tottenham to win by 7 to 1, then the gambler would have won £5 pounds plus their original stake back. Meanwhile, were the scores to be reversed to Tottenham 2 to Manchester United 4 or Tottenham 1 to Manchester United 7, then the gambler would lose their initial stake plus £1 or £5, respectively. In other words, gains and losses can far exceed their initial stake.

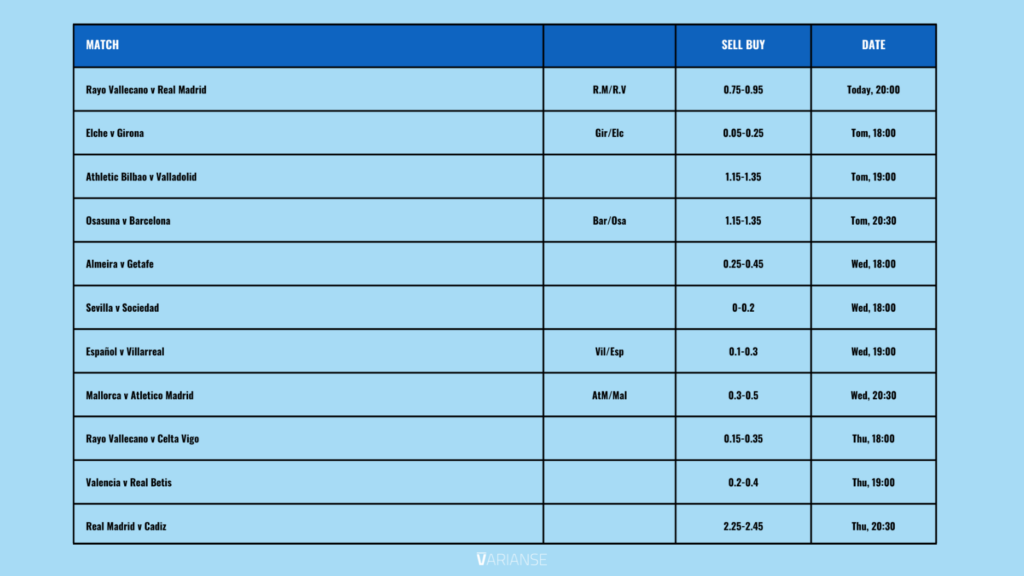

Typical Sports Spread Bet Market

Given the possibility of unlimited losses, bookmakers put a limit on how much your bet can move against you relative to your initial stake, also known as margin. Typically, losses can’t exceed 10% of the value of the bet. If losses do exceed 10% of the initial value or stake, gamblers will be prompted to pay more money to keep it open or the bookmaker will automatically close the bet at the current price. Gamblers can manage their risk by selling their stakes in a bet or set stop losses to limit their potential losses.

Financial Spread Betting

Spread betting in the financial market sense got a later start than sports spread betting, but borrows many of the same principles from the sports spread betting world. The exact beginnings of financial spread betting are pretty murky. Something similar to spread betting has been rumoured to have started in the US prior to the early 70s by some bucket shops. I suspect those rumours to be inaccurate. Laws in the US, both at the federal and state level, have always had an aversion to gambling. For instance, financial spread betting is currently banned in the US, both on the grounds it constitutes gambling and the US SEC deems financial spread betting to be a type of over-the counter derivative, which means it is prohibited for use by retail investors.

Invented by who?

Most online sources, instead, cite Stuart Wheeler as the inventor of financial spread betting. As an unemployed British stockbroker in 1974, Wheeler applied what are now known as the modern concepts of financial spread betting to the gold market. Later, as adaptation of personal computers and the internet grew, the number of firms offering spread betting services has risen dramatically. Likewise, so have the different markets people can bet and the types of bets. By the early 2000s, daily rolling bets were introduced allowing financial spread betting providers to fully mirror the underlying cash markets their bets without the need to close positions on a daily basis. Suddenly, financial spread betting was attracting day traders as much as it was traditional gamblers. Still, spread betting has remained largely a UK phenomena, because it only provides certain tax free benefits in the UK and Ireland.

Betting in Sheep's Clothes

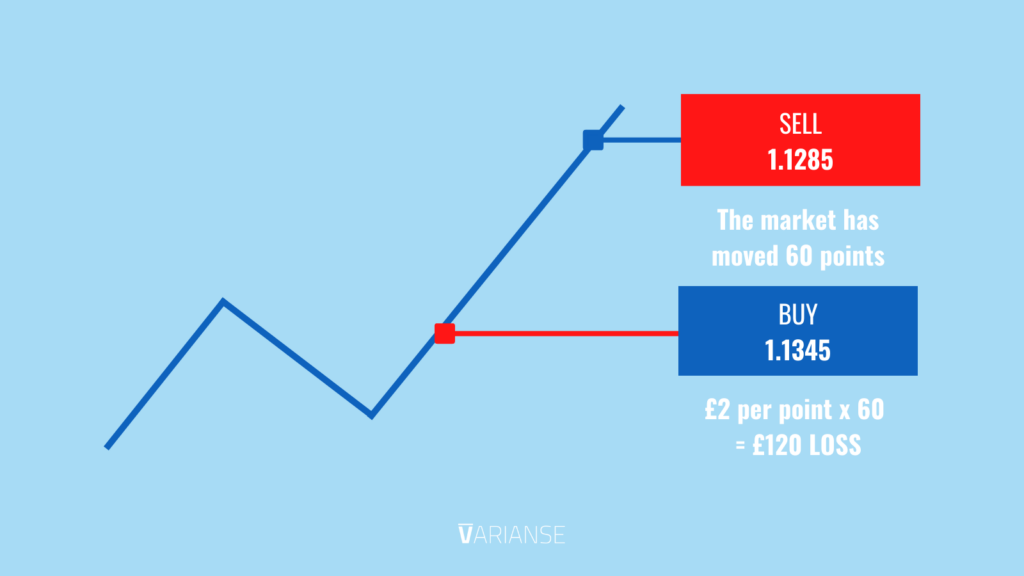

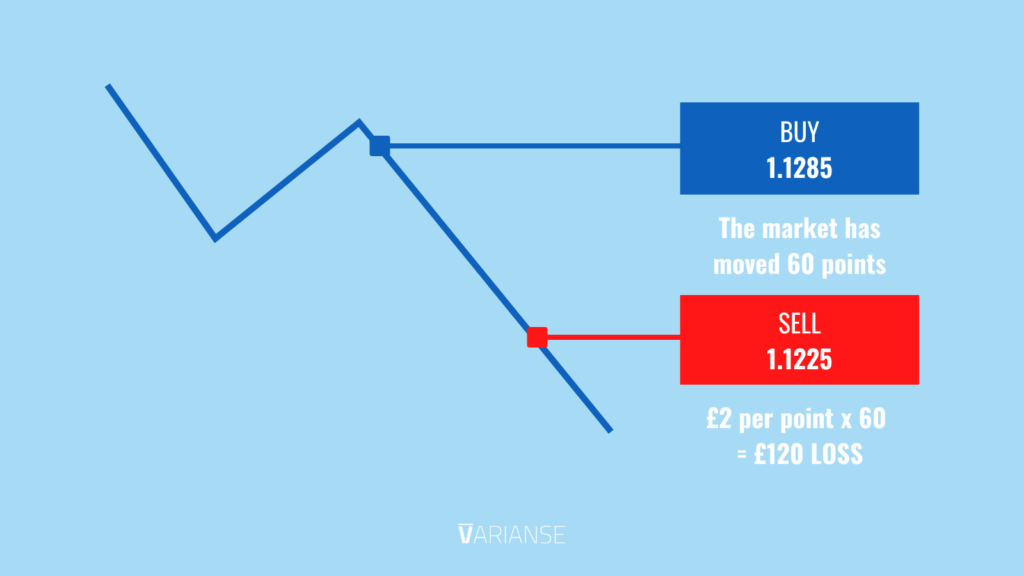

Financial spread betting inherits much from the sporting version. Traders decided how much they want to bet per unit in the underlying movement of a financial asset. Profit and loss is calculated as the difference between the opening and closing price of the bet multiplied by whatever they initially decided to bet per unit of the underlying. This is almost akin to the sports spread betting world. Margin also works in a similar, but slightly different way. With financial spread betting, traders don’t need to provide the full stake per unit upfront.

Instead, they borrow a part of the stake up front. How much they borrow depends on the initial margin requirement which is typically represented as a percentage of the total bet. Every time a someone opens a spread betting trade they are borrowing. When they leave their position open overnight they are subject to financing charges. Should an open trade position start incurring losses, just like with sports spread betting, the trader will need to deposit more cash to sustain their position or risk having it closed - also known as the maintenance margin requirement.

The glaring difference between the mechanics behind sports spread betting and financial spread betting largely deals with duration. Sporting events always have an end, whilst financial markets carry on perpetually day after day. Financial spread bets must have a fixed timescale, but they can range from a day to more than a month away. Even daily bets that roll over have some fixed end in the far in the distance. No spread betting trade is truly open ended, even though it might feel that way. Also the stated duration of a given spread betting trade does have an impact both on overnight financing costs but also the bid ask spread shown to a trader.

CFDs - Financial From the Start

At their most basic, CFDs are an over-the-counter derivative contract with your broker to pay the difference in the settlement price between the open and closing price of a trade, whether it involves equities, forex, commodities, etc. But unlike financial spread betting, CFDs have been deeply rooted in the world of British finance from its very start. Most reputable sources name Brian Keelan and Jon Wood of UBS Warburg as the inventors of CFDs, whilst working on the Trafalgar House deal in the 1990s. To this day, hedge funds and institutional investors use CFDs to both speculate and hedge their financial positions. At the start, using CFDs became particularly prominent in relation to UK share trading, because it allows both retail and institutional investors to gain exposure without having to pay UK stamp duty on share purchases.

The Internet Boom

During the 2000s and explosion of online trading, CFDs became the dejure product for online traders. Thanks to the generous sources of liquidity already laid down by participant tier-1 institutions like investment banks and funds, CFDs allow for generous direct market access to all sorts of markets without the necessity of having to own the underlying reference asset. Check out a previous blog article, where I wrote a more in depth discussion of how CFD markets work for more detailed information.

In fact, CFDs are not just for the realm of institutional and online traders. The use of CFDs have been extended to other areas of off financial market trading. For instance, CFDs have become the instrument of choice in terms of setting out green energy subsidies for renewable energy producers in the UK. Physical Brent crude oil market participants also use CFD contracts in order to manage their physical oil price exposure.

Due to US securities regulations, however, US residents are not allowed to trade in CFDs, as they are over the counter derivatives.

CFD Inner Workings

With a CFD, instead of buying or selling a unit of a tradable asset, you agree to exchange the value of an instrument’s price movement, by borrowing money to amplify any gains or losses. A CFD is very much like a total rate of return swap, a popular tool utilised by hedge funds, except for the fact that a CFD only pays once the contract is closed. CFDs are truly a financial instrument.

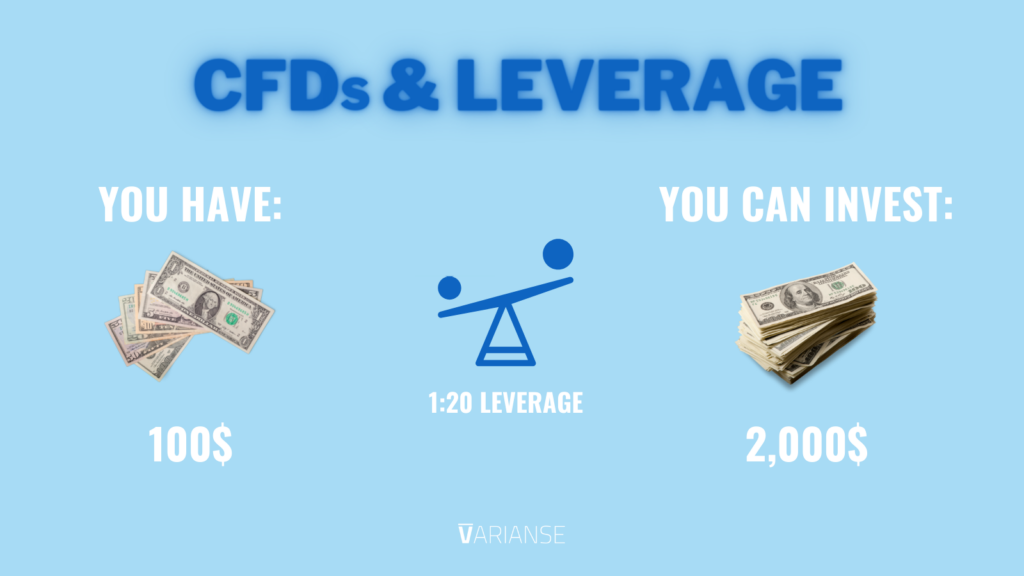

As a derivative, CFD allows traders to leverage, meaning they only need to put down a fraction of the value of their opening trade, with the rest of the value borrowed from the counterparty broker. What many new traders fail to grasp is that no matter how big the balance of their account is, when you open a CFD position you are still borrowing. That means there is always a financing cost involved when opening your trade.

Let’s say an indices trader opens a buy position of 1 lot size in the S&P 500 and their account is denominated in USD. In CFD terms, 1 lot size in an index is the equivalent to buying one index point, which is the equivalent to buying the entire index at its current level. So, if you are buying 1 lot in the S&P 500 that is currently trading at 3,848.52, then the cost of the position in USD terms is 3,848.52. If the index goes down by a point you are in loss by a dollar and if the index goes up you are in profit by a dollar.

Whether you have USD 2,000 of available equity in your account or USD 100,000, your broker will lend you the majority of the position based on the leverage they offer. For example, if your broker offers 200:1 leverage, then they will lend you USD 3.829.28 and keep USD 19.24 as collateral to support your trade, also known as the margin requirement. More equity, just means more cushion in terms of margin, in the event of adverse moves in the underlying.

Shared Advantages

Whether a trader is financial spread betting or trading CFDs, both have some advantages over trading physical assets. These include:

- Fractional position sizes (buying less than a standard contract price)

- Leverage (the ability to buy on margin)

- Ease of execution

- Ability to go long or short

- The ability to trade a wide range of international markets not necessarily directly available to a trader

- You still receive dividends in the case of shares

UK Tax Implications

I am by no account either a tax lawyer or an accountant, so I am not qualified to give tax advice. Therefore, I advise you seek professional help in regards to your personal tax affairs. That said, from what I gather off the internet, in terms of those who are solely UK tax residents, if you are a part-time trader, meaning that the majority of income comes from other activities, then CFD gains and losses are deemed as capital gains and losses according to HMRC. This means that if you have a losing year you can use those losses to offset any gains in future years. But traders will need to pay capital gains tax on their trades.

Meanwhile, for a part-time financial spread better, the HRMC views that as gambling rather than trading. As such, their profits are not taxed but neither do they receive relief for their losses.

For full-time spread betting or CFD trader, where your sole income comes from those related trading activities, then their activity is likely to be viewed as self-employment income rather than either tax free or capital gains. Again, I suggest seeking professional tax advice if you fall into this category.

Stamp duty does not apply to UK share trading using either spread betting or CFDs.

A CFD vs Spread Betting, Which Is Better?

The answer to the question does depend quite a bit on what tax situation works best for the trader. Therefore, much will depend on the tax profile of the trader. Leaving tax implications to the side, the two products share many similarities. For me personally, with the benefit of now having worked for a CFD broker, I would choose CFDs over spread betting any day. CFDs were born out of financial markets and if you use an ECN or DMA style broker, liquidity is being directly sourced from institutional participants. Spread betting isn’t really utilised by institutions, so if you are trading through a spread better, there really is a third party involved in showing the prices you see on your platform.

CFDs trading is also more true to form relative to trading the underlying physical. Rather than size your positions by point with spread betting, CFDs actually involve buying and selling position sizes just as you would do if you were trading the underlying instrument. In addition, I personally found it much easier to negotiate trading spreads and commissions, and other aspects of my trading conditions with CFD providers than I have when spread betting. The bottom line is CFD trading is just a bit more professional.

The Best of Both Worlds

Here at VARIANSE, we make it possible to benefit from the best CFD trading conditions and still enjoy “spread betting” status by deeming your CFD account as a gambling rather than a trading account. We simply do this through a side letter with your account opening process. Come and find out why we were twice awarded the Best Broker for Execution in 2021. New live cTrader accounts also benefit from a one time 25% off purchases of algo and indicators from the ClickAlgo marketplace - ClickAlgo is the #1 provider of automated software solutions for the cTrader platform.